“Interest-free.”

Few phrases in consumer finance are more powerful.

At the checkout page of an online store, a message appears:

“Pay in 4 installments. 0% interest.”

For many shoppers, this sounds like a financial miracle. Instead of paying $200 today, you pay $50 now and the rest later. No interest, no extra cost, no visible downside.

This model—commonly known as Buy Now, Pay Later (BNPL)—has exploded globally over the past decade. Companies like Afterpay, Klarna, Affirm, and Sezzle have turned installment payments into one of the fastest-growing sectors in fintech.

But here’s the uncomfortable reality:

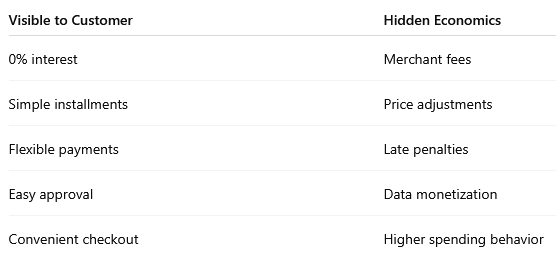

“Interest-free” payments are rarely truly free.

The cost is simply hidden somewhere else—shifted to merchants, embedded in prices, triggered by penalties, or deferred into future credit products.

To understand why “0% interest” is still profitable, we need to examine the economic machinery behind modern installment finance.

The Illusion of Free Credit

The core promise of BNPL services is simple:

- Buy something today.

- Pay in four installments.

- No interest if you pay on time.

A typical example looks like this:

- Purchase price: $200

- Pay today: $50

- Pay in 2 weeks: $50

- Pay in 4 weeks: $50

- Pay in 6 weeks: $50

No interest is added to the amount.

This seems radically different from traditional credit cards, which often charge 15–30% APR.

But businesses do not lend money for free. So the obvious question arises:

Where does the profit come from?

Revenue Source #1: Merchant Fees

The biggest hidden cost is not paid by the consumer directly.

It is paid by the merchant.

Retailers that offer BNPL options typically pay a 2–8% transaction fee to the BNPL provider.

For example:

The BNPL company keeps the difference.

Why would retailers agree to such high fees—higher than normal credit card processing?

Because BNPL increases sales.

Studies show merchants often see:

- 20–30% higher conversion rates

- Larger average order values

In other words:

Customers buy more when the payment pain is delayed.

Retailers happily pay the fee because the alternative is losing the sale entirely.

Revenue Source #2: Higher Retail Prices

Although merchants technically pay the BNPL fees, consumers often absorb the cost indirectly.

Retail businesses operate on thin margins. If offering installment payments adds a 4–8% cost, that cost must eventually be recovered.

This usually happens through:

- Slightly higher product prices

- Reduced discounts

- Increased margins across all products

Some analysts estimate retailers using BNPL increase baseline prices by 3–7% to compensate.

This means even customers who do not use BNPL may still pay for it.

The cost is distributed quietly across the entire retail ecosystem.

Revenue Source #3: Late Fees

The second major revenue stream comes from penalties.

Most BNPL platforms advertise zero interest only if payments are made on time.

Miss a payment, and the picture changes.

Typical fees include:

- $5–$15 late payment fees

- account reactivation fees

- payment rescheduling fees

While each fee may seem small, the effective interest rate can be enormous.

Example:

- Installment payment: $25

- Late fee: $10

That is effectively a 40% charge on the missed installment.

Across millions of users, these fees become a significant revenue source.

Revenue Source #4: Longer-Term Financing

Many BNPL platforms offer a second type of loan beyond the typical “pay in four” plan.

These are longer installment loans, often used for larger purchases such as:

- electronics

- furniture

- travel

- home improvement

Unlike short-term plans, these loans often do carry interest.

For example, some extended financing options may charge 7.99% to 29.99% APR depending on credit risk.

This creates a powerful customer funnel:

1. Start with “interest-free” purchases.

2. Build trust with the platform.

3. Eventually use larger financed loans.

The “free” product becomes a customer acquisition tool.

Revenue Source #5: Interchange Fees

Some BNPL companies now issue payment cards or digital wallets.

These generate interchange fees—small charges paid by merchants whenever a card transaction occurs.

Even if the consumer pays no interest, the payment network produces revenue through:

- card processing fees

- network settlement fees

- banking partnerships

These micro-fees accumulate across millions of transactions.

Revenue Source #6: Data and Marketing Value

BNPL companies also act as powerful shopping platforms.

They collect vast amounts of data about consumer behavior:

- spending patterns

- brand preferences

- purchase timing

- credit reliability

This information helps retailers target customers more effectively.

BNPL platforms increasingly monetize this through:

- sponsored product placements

- affiliate marketing

- targeted promotions

In this model, BNPL becomes not just a lender—but a retail marketing channel.

The Behavioral Economics Behind BNPL

Perhaps the most important driver of BNPL profitability is psychology.

Humans perceive payments differently depending on how they are structured.

A $200 purchase feels expensive.

Four $50 payments feel manageable.

Research suggests around 70% of BNPL users admit they spend more than they would have otherwise.

This is called the “payment decoupling effect.”

The pain of paying is separated from the moment of purchase.

As a result:

- spending increases

- impulse buying rises

- multiple installment plans accumulate

Consumers often underestimate how many obligations they have open simultaneously.

The Risk of Stacked Debt

Another hidden risk of BNPL is loan stacking.

Because many BNPL loans do not always appear immediately on credit reports, consumers may take out several at once.

Example:

- Clothing purchase: $80

- Electronics purchase: $400

- Furniture purchase: $300

- Vacation booking: $600

Each one is split into installments.

Individually they seem manageable.

Combined, they can overwhelm a monthly budget.

In fact, surveys show about 24% of BNPL users fell behind on payments in 2024, highlighting the growing debt risk.

Why “Interest-Free” Works as Marketing

From a financial perspective, “interest-free” financing is one of the most powerful marketing strategies ever created.

It works because it:

1. Removes psychological resistance to borrowing

2. Simplifies decision-making

3. Frames credit as harmless

Consumers rarely analyze the full financial system behind the offer.

They simply see:

“No interest.”

In reality, the economic structure is more complex:

The Broader Shift in Consumer Finance

BNPL is not just a payment option.

It represents a broader transformation in financial services.

Traditional credit models relied on interest income.

Modern fintech increasingly relies on:

- transaction volume

- behavioral data

- platform ecosystems

- embedded finance

Instead of charging borrowers directly, companies monetize the entire shopping experience.

The result is a financial product that feels frictionless—but is deeply embedded in retail economics.

Conclusion: Nothing in Finance Is Truly Free

Interest-free payments are not a scam.

But they are also not what they appear.

The cost of financing is simply redistributed:

- merchants pay fees

- retailers raise prices

- late users pay penalties

- some customers take higher-interest loans later

In the end, someone always pays.

The genius of the BNPL model is that the cost becomes invisible.

Consumers see convenience.

Retailers see higher sales.

Fintech companies see massive transaction volume.

And the phrase “interest-free” continues to do its quiet work—turning everyday purchases into small loans, hidden inside the checkout button.

Is the Global Pension System Headed Toward Crisis?

When Machines Control the Market

When Governments Become the Largest Debtors

Why global investment flows increasingly concentrate wealth in a few cities

Why the Yield Curve Predicts Recessions

What Makes Financial Systems Stable or Fragile?

How weaponized finance is changing international monetary relations

Why traditional insurance models may struggle in a volatile century

Should all forms of profit be acceptable in financial markets?